Navigating the complexities of student loans can be a daunting task for many.

MyFedLoan, a servicer contracted by the U.S. Department of Education, offers a comprehensive solution for managing federal student loans.

Understanding how to use MyFedLoan effectively is crucial for borrowers seeking to maintain financial health and make informed decisions about their education financing.

This Logintrick guide aims to demystify the intricacies of MyFedLoan, a platform used by millions of students to manage their federal student loans

Due to a technical issue, we cannot provide the login link. We’ll share it as soon as it’s available again.

Overview of MyFedLoan

MyFedLoan plays a crucial role in managing federal student loans, handling everything from billing and payment processing to customer service.

As a key part of the Federal Student Aid (FSA) program, it operates under a contract with the U.S. Department of Education.

This service ensures that borrowers receive comprehensive support in managing their student loans, making the process smoother and more efficient.

With its focus on effective loan servicing, MyFedLoan is an essential resource for students navigating their financial obligations after college.

Key Functions and Features

- Account Management:

- Online Account Access: Borrowers can create and access their accounts online to manage their student loans.

- Loan Tracking: MyFedLoan provides tools to track loan balances, payment history, and accrued interest.

- Repayment Plan Management:

- Selection of Repayment Plans: Offers a variety of federal loan repayment options, including Standard, Graduated, Extended, Income-Driven Repayment (IDR) plans, and others.

- Repayment Plan Adjustment: Borrowers can request changes to their repayment plans as their financial situations evolve.

- Processing Payments:

- Payment Processing: Manages the processing of regular loan payments, including setting up automatic payments.

- Extra Payment Allocation: Allows borrowers to specify how extra payments are applied to their loans.

- Customer Support and Guidance:

- Customer Service: Provides customer support to assist with loan-related questions and issues.

- Educational Resources: Offers educational resources about student loans and repayment options.

- Deferment and Forbearance:

- Assistance During Hardship: Assists with applications for deferment or forbearance in cases of financial hardship, unemployment, or other qualifying situations.

- Loan Forgiveness Programs:

- Public Service Loan Forgiveness (PSLF): Manages applications and tracks qualifying payments for borrowers pursuing PSLF.

- Teacher Loan Forgiveness: Administers loan forgiveness for eligible teachers.

- Consolidation:

- Loan Consolidation Assistance: Provides information and assistance for borrowers looking to consolidate multiple federal student loans into a single loan.

Navigating MyFedLoan: A Users’ Guide

Navigating MyFedLoan effectively is crucial for managing your federal student loans.

Here’s a detailed guide on how to create and access an account, along with an overview of the dashboard and its main features:

Creating and Accessing a MyFedLoan Account

- Visit the MyFedLoan Website: Start by navigating to the official MyFedLoan website. Ensure you’re visiting the correct and secure site to protect your personal information.

- Account Registration: On the homepage, look for an option to register or create a new account. This usually involves verifying your identity and setting up login credentials.

- Verification: You’ll likely need to provide personal information such as your Social Security Number, date of birth, and possibly loan details to verify your identity.

- Username and Password: Choose a username and password. It’s important to create a strong, unique password for security.

- Set Up Security Features: MyFedLoan may require or offer additional security features, such as security questions or two-factor authentication, to enhance the protection of your account.

- Login to Your Account:

- Once registered, you can log in using your chosen username and password.

- If you encounter login issues, use the provided “Forgot Username/Password” links or contact customer service for assistance.

Overview of the Dashboard and Main Features

- Dashboard Interface: After logging in, you’ll be directed to the dashboard, which provides a comprehensive overview of your loan details and management tools.

- Loan Summary: This section displays your total loan balance, individual loan details, and the status of each loan (e.g., in repayment, in deferment).

- Repayment Plan Management:

- Plan Overview: You can view your current repayment plan and projected payoff dates.

- Change Plans: There’s an option to explore and switch to different repayment plans, including income-driven repayment options.

- Payment Processing:

- Make a Payment: You can make payments directly from the dashboard, set up automatic payments, or explore alternative payment methods.

- Payment History: Review your past payments, including amounts and dates.

- Communication Center:

- Inbox: Access important messages, documents, and notifications from MyFedLoan.

- Document Upload: Submit required documents or forms directly through your account.

- Tax Information: Access tax documents, such as your 1098-E student loan interest statement, which is important for tax filing purposes.

- Deferment and Forbearance Requests: If you’re facing financial hardship, you can explore options for deferment or forbearance and apply directly through the dashboard.

- Loan Forgiveness Applications: For borrowers pursuing Public Service Loan Forgiveness or other forgiveness programs, you can track your qualifying payments and submit the necessary forms.

- Account Settings: Update personal information, manage security settings, and customize your account preferences.

Tips for Effective Navigation

- Regular Check-Ins: Regularly log in to your account to stay updated on loan statuses and any new messages or documents.

- Utilize Resources: MyFedLoan provides various resources and tools; make use of them for effective loan management.

- Stay Informed: Keep yourself updated on any changes to federal student loan policies or terms that might affect your loans.

Navigating MyFedLoan is a key aspect of managing your student loans.

Familiarizing yourself with the dashboard and utilizing the available tools and resources can significantly help in keeping track of your loans and making informed decisions about repayment.

Loan Repayment Plans

Navigating through loan repayment plans, particularly for federal student loans managed by services like MyFedLoan, is crucial for borrowers.

Understanding the different types of plans available and how to choose the right one for your needs can significantly impact your financial well-being.

Here’s a detailed look at the various repayment plans and guidelines for selecting the most suitable one:

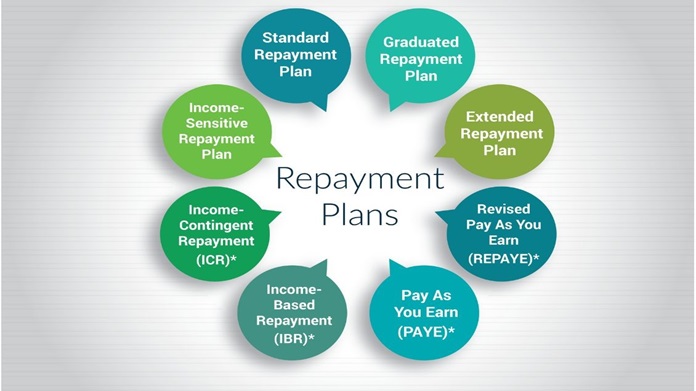

Types of Federal Student Loan Repayment Plans

- Standard Repayment Plan:

- Term: 10 years (up to 30 years for Consolidation Loans).

- Payments: Fixed amount, ensuring the loan is paid off within the term.

- Suitable For: Those who can afford standard payments; results in less interest paid over time.

- Graduated Repayment Plan:

- Term: 10 years (up to 30 years for Consolidation Loans).

- Payments: Start lower and increase every two years.

- Suitable For: Borrowers who expect their incomes to increase over time.

- Extended Repayment Plan:

- Term: Up to 25 years.

- Payments: These can be fixed or graduated.

- Eligibility: Borrowers with more than $30,000 in Direct Loans or FFEL Program loans.

- Suitable For: Those seeking lower monthly payments, though they’ll pay more in interest over time.

- Income-Driven Repayment Plans:

- Types: Includes Income-Based Repayment (IBR), Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), and Income-Contingent Repayment (ICR).

- Payments: Based on your income and family size, typically 10-20% of your discretionary income.

- Term: 20-25 years, after which any remaining balance may be forgiven.

- Suitable For: Those with a high debt-to-income ratio; offers potential loan forgiveness after the repayment period.

- Income-Sensitive Repayment Plan:

- Available For: FFEL Program loans only.

- Payments: Based on annual income, adjusting annually.

- Term: Up to 10 years.

- Suitable For: Borrowers with FFEL loans seeking income-based payments.

How to Choose the Right Plan?

- Assess Your Financial Situation: Evaluate your current income, expenses, and financial goals. Consider your job stability and potential for income growth.

- Estimate Future Earnings: Consider your career trajectory and whether you expect your income to increase significantly over time.

- Consider Your Debt-to-Income Ratio: High debt with a lower income may make income-driven plans more appealing.

- Use Loan Simulators: Utilize loan repayment calculators or simulators provided by services like MyFedLoan or the Federal Student Aid website. These tools can help you estimate monthly payments under different plans.

- Factor in Loan Forgiveness: If working in public service or a qualifying profession, income-driven plans might be more beneficial due to potential loan forgiveness.

- Consult a Financial Advisor: For complex situations, consider seeking advice from a financial advisor knowledgeable in student loans.

- Review Annually: Your financial situation can change. Review and adjust your repayment plan annually or as needed.

- Contact Your Loan Servicer: If in doubt, contact your loan servicer (like MyFedLoan) for guidance and clarification on each plan’s terms and conditions.

Tips for Effective Loan Management

Effective loan management is crucial for handling student debt responsibly and maintaining financial health.

Here are detailed tips and best practices for managing student loans, along with advice on avoiding common pitfalls:

Best Practices for Managing Student Loans

- Understand Your Loans:

- Know the Details: Be clear about your loan amounts, interest rates, and repayment terms. Understand the differences between federal and private loans.

- Read the Fine Print: Pay attention to the terms and conditions of your loans, including grace periods and any benefits like interest rate reductions for automatic payments.

- Organize Your Documents: Keep all loan-related documents, including communication from your loan servicer, in an organized manner for easy reference.

- Use Online Tools and Resources: Utilize online platforms like MyFedLoan for federal loans to track balances, make payments, and access important documents.

- Choose the Right Repayment Plan: Select a repayment plan that fits your financial situation. Income-driven plans can be beneficial for those with lower earnings, but standard plans can save on interest costs over time.

- Consider Consolidation or Refinancing: Loan consolidation can simplify payments, and refinancing may offer lower interest rates. However, weigh the pros and cons, especially the potential loss of federal loan benefits if you refinance with a private lender.

- Make Payments on Time: Avoid late fees and negative credit impacts by making timely payments. If you can’t make a payment, contact your loan servicer immediately to discuss options.

- Pay More Than the Minimum: If financially possible, pay more than the required minimum to reduce the principal faster and save on interest.

- Utilize Grace Periods and Deferments Wisely: If you have a grace period or qualify for deferment, use this time to plan your repayment strategy or to save up for future payments.

- Stay Informed About Changes: Keep up-to-date with any changes in student loan policies or relief programs that may affect your loans.

- Communicate with Your Loan Servicer: Stay in regular contact with your loan servicer, especially if you encounter financial difficulties. They can provide guidance and help you explore options like deferment, forbearance, or alternative repayment plans.

Avoiding Common Pitfalls

- Ignoring Your Loans: Not addressing your loans or ignoring communications from your loan servicer can lead to default, damaging your credit score and leading to additional fees.

- Accruing Unnecessary Interest: Avoid capitalization of interest, which can occur when unpaid interest is added to your principal balance, typically after periods of deferment or forbearance.

- Falling for Scams: Be wary of companies that promise loan forgiveness or drastically lower payments for a fee. Genuine assistance and advice regarding your federal loans are available for free through your loan servicer.

- Over-borrowing: Only borrow what you need for education costs to avoid excessive debt. Carefully consider the return on investment of your education and potential future income.

- Neglecting Savings and Emergency Funds: While focusing on loan repayment is important, don’t neglect building an emergency fund and saving for retirement or other financial goals.

Final Words

MyFedLoan is a critical service for borrowers of federal student loans, offering comprehensive management, repayment options, and support services.

Its role in facilitating loan repayment and offering solutions tailored to individual financial situations is essential in helping borrowers successfully manage their student loan debt.